Canadians pay a lot in taxes. Among the 38 members countries of the Organisation for Economic Co-operation and Development (OECD), Canada had a tax-to-GDP ratio of 34.4% in 2020, compared with the OECD average of 33.5%. The Fraser Institute declared Tax Freedom Day on June 15, 2022, which they define as follows:

“If you had to pay all your federal, provincial and municipal taxes up front, you would give government every dollar you earned from January 1st to Tax Freedom Day, when Canadians finally start working for themselves. In 2022, the average Canadian family (with two or more people) will pay 45.2 per cent of its annual income in taxes, including income taxes, payroll taxes, health taxes, sales taxes, property taxes, fuel taxes, carbon taxes, and more.”

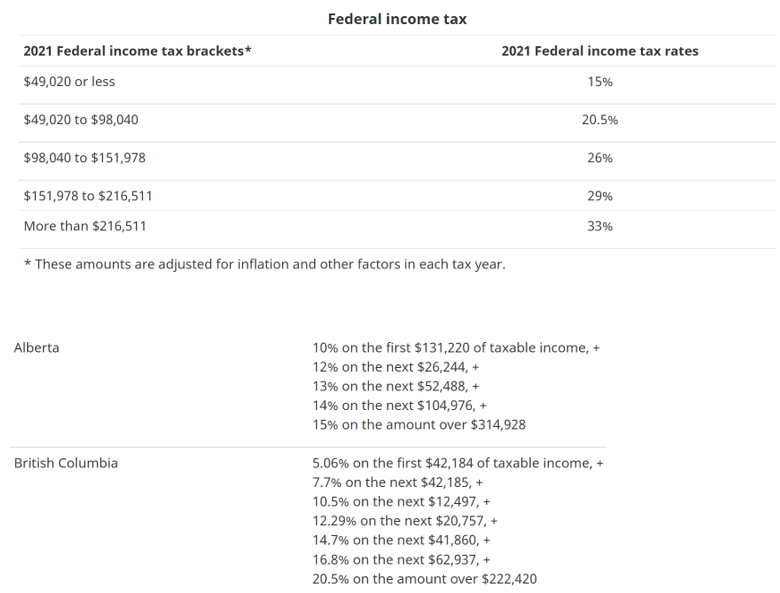

And income taxes are responsible for a good portion of those tax funds, as is evident in the income tax numbers posted at the end of this article.

Most would agree that working until June 15th before getting to enjoy the income fruit of your labour is not a scenario that we dream of as children, as we’re planning for a future career as a doctor, or teacher, or space cowboy. But there are ways to reduce this tax burden, and one of the best ways is through income splitting.

What is Income Splitting?

“Simply put,” WealthCo Senior Planner Ryan Mackiewich explains, “income splitting is taking one person’s income and sharing it with another person.”

Income splitting is a tax strategy used by many Canadians to reduce their overall tax liability.

“By transferring income from a high-income earner to a low-income spouse or dependent,” Mackiewich explains, “taxpayers can take advantage of lower marginal tax rates and receive other benefits such as increased government benefits and credits.”

This act of transferring income from a higher-earning spouse to a lower-earning spouse, means the total household income is divided into two lower taxable brackets, resulting in a reduction in the overall amount of taxes paid. Income splitting can be especially beneficial for families with children, as the lower-earning parent may be able to claim various childcare credits and deductions.

Recent Changes to Income Splitting

In December 2017, the Canadian government implemented a new set of rules, known as the "tax on split income" (TOSI), that limits the ability to income split.

“Prior to the TOSI rules, there were many legal and accepted ways to split income,” Mackiewich explains. “There were more ways to split or share property income, business income, personal income, and investment income. Under TOSI, only certain types of income can be split. There has been a big impact to small family businesses (common with professional service providers like doctors, lawyers, accountants) where income was split. These rules changed to allow income splitting only when someone worked a sufficient amount in the business or reached a certain age.”

Additional impacts from TOSI include:

- Limitations on how certain types of income, such as dividends from private corporations, can be split;

- Exclusions for taxpayers under the age of 18 and for certain family trusts;

- May prevent parents from claiming childcare expenses; and

- Can affect estate planning - for example, TOSI may limit the ability to transfer assets to family members at a lower tax rate.

How You Can Make Income Splitting Work For You

While income splitting can be a beneficial way to reduce taxes, it is important to be aware of the rules and restrictions that apply in order to avoid penalties. For example, knowing what types of income are eligible for splitting, and understanding the limits on the amount that can be transferred. As well, income splitting may not be advantageous in all cases, such as when both spouses have similar incomes.

“While income splitting is perfectly legal, it can be complex and should only be undertaken with the help of a qualified accountant,” Mackiewich cautions. “Especially given the changes brought on by TOSI, a tax expert, such as your accountant, is your best guide for navigating these changes.”

Unclear on whether income splitting is a viable option for your unique situation? Your most trusted advisor, your accountant, can answer this question for you as well as discussing any additional tax mitigation strategies that might be worth considering.

A member of WealthCo’s Integrated Advisory community, Ryan Mackiewich, CPA, CA, FEA is a Senior Planner with WealthCo. With over 25 years as a CPA, CA providing tax and business advisory expertise, Ryan also holds the Family Enterprise Advisor (FEA) designation and applies it to working with business families to help them effectively transition business, wealth, and roles. When he’s not doing that, Ryan loves to camp, hike, and explore all the wonderful places the world has to offer.

The Integrated Advisory community consists of a network of progressive CPA firms, along with best-in-class professional advisors, service, and product specialists, who work together to deliver an elevated and holistic client experience. One that optimizes both their personal and professional lives with an integrated financial strategy designed to help clients reach their goals.

Related Posts